A variety of headwinds suggest that the party has ended for Wall Street’s artificial Intelligence (AI) adorable.

Although President Donald Trump’s trade policy has been a major topic about Wall Street over the last six weeks, it’s actually the development of artificial intelligence (AI) that’s captivated investors for over two years.

In its simplest sense, AI empowers software and systems to make decisions and take action independently and offers the ability to acquire new techniques without human supervision. It’s an innovative technology with wide-ranging applications that experts at PwC believe could boost the world’s Gross Domestic Product (GDP) $15.7 trillion by 2030.

No other company has directly profited in the AI technology than Nvidia

With the estimation of $15.7 trillion market that is addressable has the possibility of dozens, if not hundreds in winners none of the companies has enjoyed more directly the recipient of the growth of AI than the giant of semiconductors Nvidia ( NVDA 3.53 percent).

Fast forward almost overnight, Nvidia’s Hopper (H100) graphics processing unit (GPU) was adopted as the primary “brains” powering enterprise AI-accelerated data centers. It was followed with the new Blackwell GPU architecture that is able to further accelerate the computation process and is also more efficient than the predecessor.

In only two years of fiscal year (Nvidia’s fiscal year comes to an end in January, which is the month that ends) the company’s net revenues rocketed from $27 billion $130.5 billion. To give you a sense of background Wall Street’s consensus estimates for the year 2026 are 201 billion in total sales in the fiscal year 2026 (this year) and $248 billion for fiscal 2027.

Subscribe for Top Silicon Valley Tech Podcasts

Subscribe Now!With Nvidia’s incredibly fast growth rate, and the fact that there is no direct competitor has come even near to matching its blend of computing speed and efficiency in energy use, it’s no reason to be surprised to see that Wall Street analysts have rallied around the market’s AI favorite. In January, I noticed that the scores of Wall Street analysts covering Nvidia all had price targets that were more than the price at which shares were traded..

But the times are changing!!

Nvidia recently received its debut Wall Street sell rating -following the date of May 28, when Nvidia will announce its fiscal 2026’s first-quarter operational results, I expect that other analysts will follow suit.

A Wall Street analyst is bucking the popular opinion

In the middle of April Seaport Research Partners’ senior analyst Jay Goldberg initiated coverage on with a nvidia stock price goal (a Wall Street low) and a sell rating.

While Goldberg admitted that Nvidia has been doing a lot right and that its Blackwell GPU is highly sought-after and he believes that the bull case was priced in, and there were plenty of negative catalysts waiting in the waiting.

One reason is that Goldberg believes it’s going to be hard for Nvidia to meet Wall Street’s optimistic consensus expectations considering that it’s reached its capacity of orders for Blackwell in the fiscal year 2026. Even though world-leading chip fabrication company Taiwan Semiconductor Manufacturing is rapidly expanding its chip-on-wafer-on-substrate (CoWoS) capacity — CoWoS is essential for the packaging of high-bandwidth memory needed in AI-accelerated data centers — it’s still holding Nvidia back from selling even more of its next-gen hardware.

Goldberg is also anticipating that businesses are likely to take a closer look at their spending this year, and even into the 2026’s calendar year. Seaport’s senior analyst doesn’t anticipate to see an AI bubble to pop and then burst however, he believes that companies are trying to figure out the practical applications for artificial intelligence. Goldberg believes this could cause lower AI orders and spending in the next quarters to be.

Furthermore, and not unsurprisingly, Goldberg alluded to export restrictions on exports to China as a major headwind. To remind us that there was a time when the Joe Biden Administration (since October 2022) as well as the Trump administration have imposed strict export restrictions on several powerful AI chips and other equipment that is used to China. The world’s number. 2 economy according to GDP is responsible for millions of dollars annually in sales to Nvidia that could be slashed significantly in the event that tariff-related uncertainty continues to linger along with trade relations between U.S. and China sour.

But I am convinced that this is only the beginning of the iceberg. others Wall Street analysts will follow the Goldberg’s path when Nvidia takes off the cover after the bell rings at the close on May 28.

Subscribe for Top Silicon Valley Tech Podcasts

Subscribe Now!There are more sell ratings to come in Wall Street’s AI popular

Like Goldberg Similar to Goldberg, I’m glad to provide Nvidia credit for the credit it deserves. Nvidia’s Hopper as well as Blackwell chips will likely keep their advantages in computing and will remain popular hardware to use in AI Data centers. But Nvidia’s $2.9 trillion worth of valuation indicates that it will have big shoes to fill -and there are more challenges ahead than the analyst at Seaport has noted.

The most significant challenge facing Nvidia is its internal competition that it’s battling with. While the majority of analysts and investors concentrate on direct competitions like Advanced Micro Devices and Huawei but they’re not aware the fact that a large portion of Nvidia’s top clients based on net sales are developing internally AI chips and other solutions to use in their data centers.

While many of these companies stating that their internal-developed hardware will be used in conjunction with Nvidia’s GPUs, this does not change what it means that the move could result in less expensive and more easily accessible AI solutions that don’t need to be backlogged. It’s an easy way for Nvidia to lose out on the future market share in data centers.

Also, Nvidia is losing its most significant competitive advantage as well. And no I’m not talking about the speed of computation offered by Hopper as well as Blackwell. Instead, I’m referring to the advantages it’s gained due to the shortage of AI-GPUs.

While Nvidia cannot meet the huge need for its Blackwell GPU technology however, it’s not hindering AMD from bringing cheaper next-generation chips on the market. Also, it’s not hindering the internal innovations that are a part of the company’s top customers. As the hardware moves into high-performance facilities, it lowers the supply of AI-GPUs as well as the capacity to nvidia stock price that has fueled Nvidia’s profit margin.

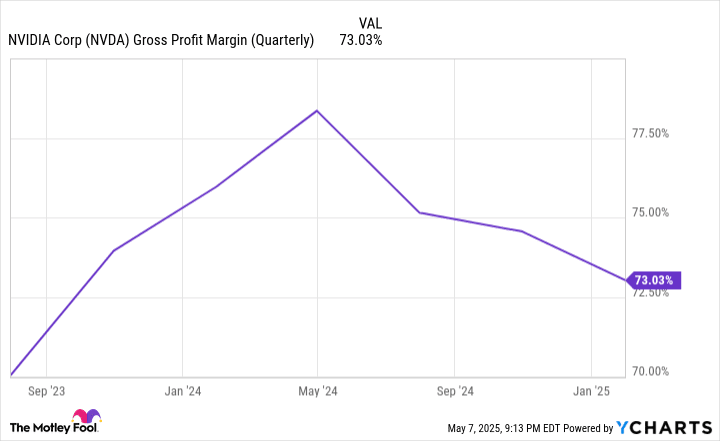

In the year prior in fiscal year 2025, Nvidia had a sweltering-hot generally accepted accounting standards ( GAAP) gross margin of 78.4 percent. Since then, the GAAP gross margin has been declining each quarter and is predicted to drop to 70.6% (or 70.6 percentage (+/- 50 basis points) for the first quarter of fiscal 2019 to be reported the 28th of May. It’s evident that Nvidia’s biggest advantage disappearing in front of our faces.

Finally, the past will strongly suggest it is likely that artificial intelligence isn’t immune to an event that bursts a bubble. Every new technology or innovation for the last 30 years has experienced an initial bubble during its expansion phase. The overwhelming majority of companies are not optimizing the effectiveness of their AI strategies, and producing a positive return on their AI investments, it seems that investors overestimated the initial value of an innovative technology that could revolutionize the way we work.

As the more Wall Street analysts begin paying at these aspects I expect that the amount of ratings indicating sell for Nvidia stock will rise.

Don’t miss your chance to take advantage of a lucrative opportunity

Do you feel as if you’ve missed the boat when investing in the best stocks? You’ll be interested in hearing this.

Rarely our expert team of analysts will issue an occasional “Double Down” stock recommendation for companies they believe are on the verge of rise. If you’re worried that you’ve missed the opportunity to invest, this is the moment to make a purchase before it’s too for you to wait. The statistics speak for themselves.

- Nvidia If you had invested $1,000 in 2009 and doubled that to 2009 in Nvidia, you’d be able to get $302,503! *

- Apple If you put in $1,000 at the time we doubled it to 2008 in the year that was, you’d be left with $37,640! *

- Netflix If you put in $1,000 when we doubled our investment to a maximum of $4,000 in 2004 you’d get $614,911! *

In the present, we’re releasing “Double Down” alerts for three amazing businesses, and there might never be another chance similar to this in the near future.